Today I went to the launch of a bank. Now there’s something you don’t say everyday… or maybe you do? Australia’s banking market is so crowded that on average every single adult has at least three active accounts & relationships with seperate banks. So while to launch a new bank in what is an extremely saturated market might seem like madness to us, to Dom Pym and ex AFL coach Grant Thomas, co-founders of Up, creating a bank that was designed around “living” seemed like something they had to do.

“Disruption isn’t the reason for us to do it.”, Pym tells me at the typically wet weathered Melbourne launch. “It will be the rhetoric used, but our goal is to create technology led banking and not banking led technology. There’s a subtle difference there but it’s a big one.” And Pym should know, he’s worked in the banking sector for decades. The co-founder of Pin Payments and also banking software development house Ferocia, his team has worked closely on projects involving Australia’s big four banks and was responsible for Bendigo Bank’s digital infrastructure.

Pym & Ferocia’s relationship with Bendigo Bank is an important one. It’s what allows Up to exist. Whilst completely independent from Bendigo Bank it still relies on the bank to serve as its encumbered underwriter. Customer’s money will be secured by Bendigo but that is where the relationship begins and ends as Up’s products, or “superpowers” as they eye-rollingly like to call them, differ in almost every way.

For a start, getting an account with Up is as simple as downloading their app, entering your name and verifying your ID. From there you not only have access to a fully functioning account with your BSB & account details right in front of you, for iOS users (and very soon Android ones too), you’ll also have ApplePay setup and ready to go. No waiting for a card to arrive in the mail (although one will soon), no filling out forms and jumping through verification hoops, just BAM, an account ready to use in what takes an average of around two and a half minutes.

One of the new bank’s most impressive features at launch is called “Naked Truth“. It’s a very smart and feature-rich version of your old school statement that whilst most players now bless us with a more up to date transactional history Up’s goes to a whole new level. Up describes it as “complete clarity on when, where and how you spend your money” and that sums it nicely.

For a start, instead of seeing weird business names that mean absolutely nothing to anyone you’ll see the name of the actual cafe you bought your coffee in. They do this through a combination of crowd sourcing and business partnerships that allow them to nail down exactly where and whom you bought something from instead of using their unruly bank registered merchant details. They’ll also record the location of your phone (if you allow it) and time of day the actual transaction took place at, so even if the true name isn’t available you can better track down where you spent your money and on what instead of freaking out and starting to cancel your cards because you think someone’s stolen your details.

Once in your transaction history every transaction you make is group against the seller meaning you can now see how much you’re spending on your coffees at the local cafe each month, or get the shock of your life when you see how much you’ve spent altogether. It sounds simple but they’re features you just don’t have with your current bank and when you see how quick and easy it is you’ll wonder why they’ve been so long coming.

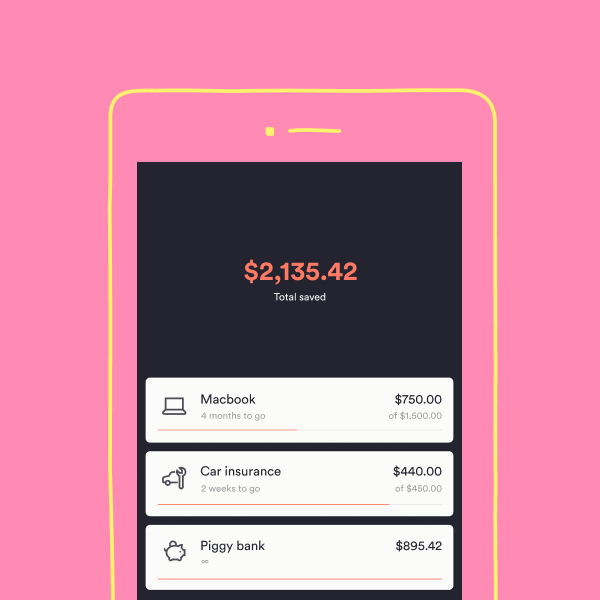

Another of the superpowers is called “Life Savers“. This is Up’s take on savings accounts but with a twist. There’s no limit to the number of savings accounts you have for instance. There’s no minimum balance requirement or penalty for withdrawing from them at any time. They provide the same 2.75% introductory interest rate (for balances up to $50k) across all of the savings accounts you create but you don’t have direct access to deposit to them, that’s facilitated through your main transactional account. That’s because, from what I can tell, they’re technically all the same account. You’re only ever given a single BSB and account number so what it appears they’re doing is a little magic to essentially break that one account into many and showing you the result. Tricky, but clever.

Another of the superpowers is called “Life Savers“. This is Up’s take on savings accounts but with a twist. There’s no limit to the number of savings accounts you have for instance. There’s no minimum balance requirement or penalty for withdrawing from them at any time. They provide the same 2.75% introductory interest rate (for balances up to $50k) across all of the savings accounts you create but you don’t have direct access to deposit to them, that’s facilitated through your main transactional account. That’s because, from what I can tell, they’re technically all the same account. You’re only ever given a single BSB and account number so what it appears they’re doing is a little magic to essentially break that one account into many and showing you the result. Tricky, but clever.

The savings accounts are created with goals in mind. Emergency funds, buying a new laptop, a holiday. The idea is for one to be created with a target figure set that you work to achieve. The system aids in that by incorporating a “round-up” feature that we’ve seen other providers do but having it all in the one system and represented within your transactional history is a big advantage for Up.

The last of the main launch features is “Kill Bills” and while it was a big part of the pitch and technically remarkable I was the least convinced by.

The last of the main launch features is “Kill Bills” and while it was a big part of the pitch and technically remarkable I was the least convinced by.

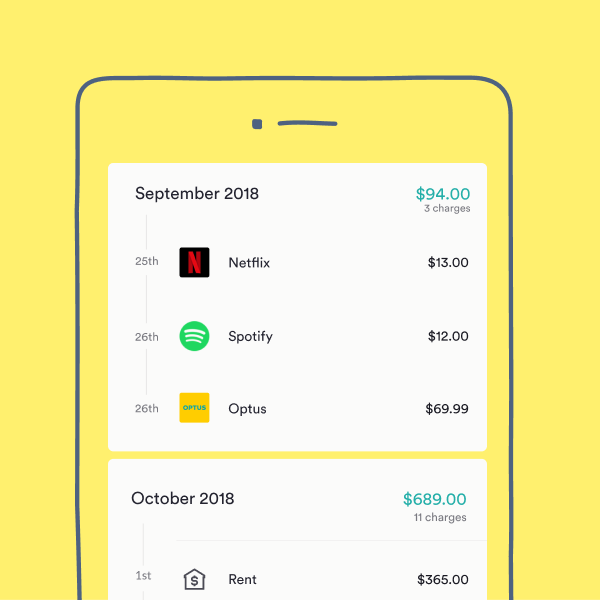

The idea is for Up to essentially identify billing subscriptions you have. Perhaps it’s a Netflix account or a Spotify one, maybe your mobile phone bill and so on & so forth. From there they’ll appear in a seperate tab within the app that identifies them and is smart enough to only show the subscription portion of the provider and not include any ad-hoc purchases. For example with Apple it might include your Apple Music subscription but wont incorporate movie rentals or Mac purchases.

The future of this feature is to show the user a “spending balance” on their account. One that takes into account all your subscriptions, saving plans and pending payments to show what you can spend without going into the red. It’s budgeting, but for millennials.

For right now, it’s a list of your subscriptions, which is fine and you have the ability to identify one that you perhaps forgot about and then cancel them yourself, that’s cool but you can’t actually pay a bill, there’s no BPAY or way of doing that. Yet.

At its core Up provides a banking service that’s built for a new generation of users. Everyone I’ve spoken to about it and demoed their app to is immediately impressed. It’s easy and friendly to use, which they all love, but the want to switch banks is something almost all of them feared. Even with the speed and simplicity of creating an account with Up, the thought of migrating existing direct debits and details with employers is something that could put Up in the “too-hard” basket.

Trust is another hurdle for the Up team will need to overcome. They’re off to a good start being very upfront about their relationship with Bendigo Bank whom have a track record far more appealing than many of the other banks in Australia at the moment. They’re also an Australian based team both in technical and service support, the technical side being handled by the Ferocia team in South Melbourne and the service by Bendigo Bank’s professionals.

It’ll be an interesting journey to see how Up fares in this new age of digital banking and whilst they’re hardly the only fin-tech in the startup space they are one of the first to market and they’ve done so off of their own backs, with years of experience in the banking sector and no outside VC funding or boards to speak of.

UPDATED 10/10/18 12:45

We incorrectly stated the introduction interest rate applied to all accounts including the main transactional one. The rate only applies to savers.

Regulars/subscriptions cannot be cancelled via the app currently. This is a feature coming soon.